Tax Law Blog

Expert insights on IRS tax resolution, criminal tax defense, and compliance from our attorneys.

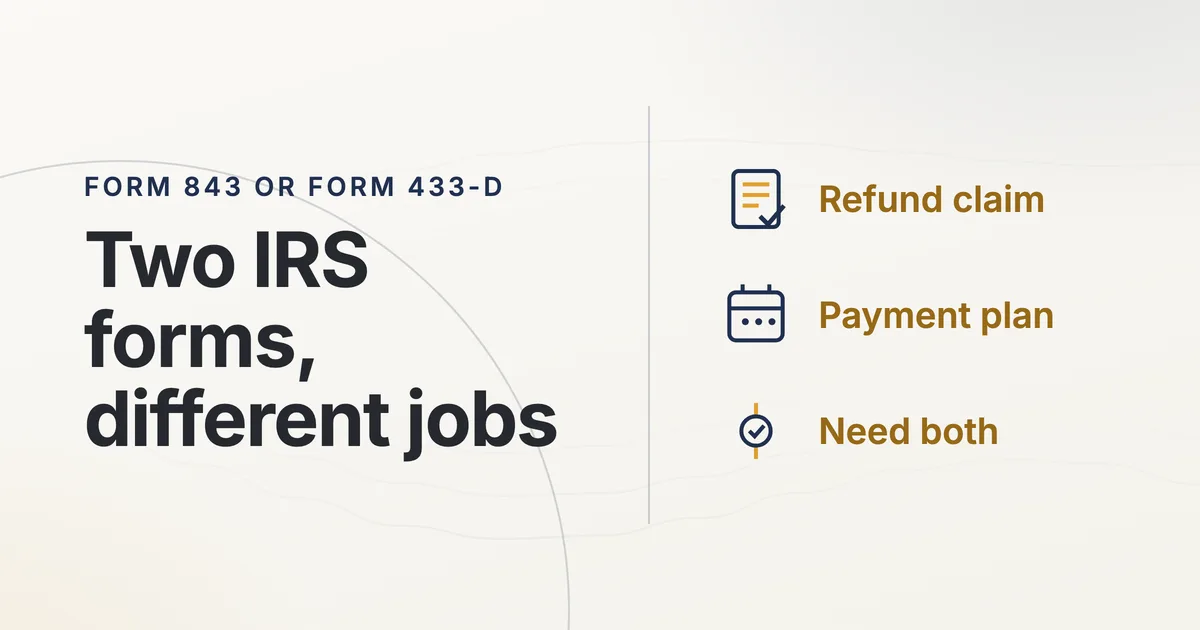

IRS Form 843, How to File It and When Form 433-D Is the Right Form Instead

What IRS Form 843 asks for, what to attach, where to mail it, and how to tell when your case actually calls for Form 433-D instead.

IRS Audit of a $3 Million Lottery Prize Resolved With No Additional Tax or Penalties

Our firm recently represented a taxpayer in an IRS examination that began with a $3 million lottery prize and an amended federal income tax return prepared and filed before we were involved. The examination closed with no additional tax, no penalties, and the taxpayer's original tax liability left u

McCauley Law Attorneys Published in the Maryland Bar Journal

The Maryland Bar Journal, published by the Maryland State Bar Association, has featured an article written by two of our attorneys, Daniel S. Heller, Esq. and Seth E. Goldstein, Esq. The article, "The Rise of AI: Revolutionizing Tax Law and Beyond," appears on page 93 of the latest edition. The piec

Why Conventional IRS Defense Breaks Down. And What Actually Stops Collections

The IRS collected more than $4.7 trillion in taxes during fiscal year 2023, according to the IRS Data Book. And the enforcement machinery behind that number doesn't pause for confusion, fear, or a busy season at your business. If you're already dealing with notices, a lien on your property, or a gar

How Tax Resolution Actually Works: The Methodology Behind Getting the IRS Off Your Back

The IRS collected more than $104 billion through enforcement actions in a recent fiscal year, according to the IRS Data Book. And the overwhelming majority of that came from people who either didn't respond in time or didn't know what options they had. If you're sitting on a tax debt right now, that

When to Act and When to Wait: Timing Decisions in IRS Defense That Actually Matter

The IRS collection machine doesn't pause while you weigh your options. Notices stack up, deadlines pass quietly, and the window for your best resolution narrows. Not because the IRS is aggressive, but because the system is designed to move forward whether you're ready or not. The right time to act o

Passport Renewal Denied? How McCauley Law Offices, P.C. Can Get You Back on Track

Imagine planning that dream vacation or essential business trip, only to have your passport renewal rejected due to an IRS flag. It's a frustrating wake-up call, but it's also an opportunity to resolve underlying tax issues once and for all. At McCauley Law Offices, P.C., we

Why the IRS Restricts Passport Renewals for Delinquent Taxpayers – And How to Check Your Status

Traveling abroad should be about adventure and relaxation, not anxiety over tax troubles. At McCauley Law Offices, P.C., we've seen how IRS certifications can derail plans by linking tax debts to passport restrictions. This post explores why the IRS imposes these rules, the practical

Understanding the IRS's "Seriously Delinquent Taxpayer" Status and Its Implications

At McCauley Law Offices, P.C., we specialize in helping individuals navigate complex tax issues with the IRS. One increasingly common problem we encounter is the designation of a taxpayer as "seriously delinquent." This status can have far-reaching consequences, including restric

What IRS Tax Help Actually Looks Like: Real Timelines, Honest Outcomes, and What Success Means

The stack of IRS notices on your desk isn't getting smaller, and the number at the top isn't getting lower. Every week you wait, penalties compound, interest accrues, and the IRS moves one step closer to taking action you can't easily reverse. Real IRS tax help isn't about making the debt disappear.

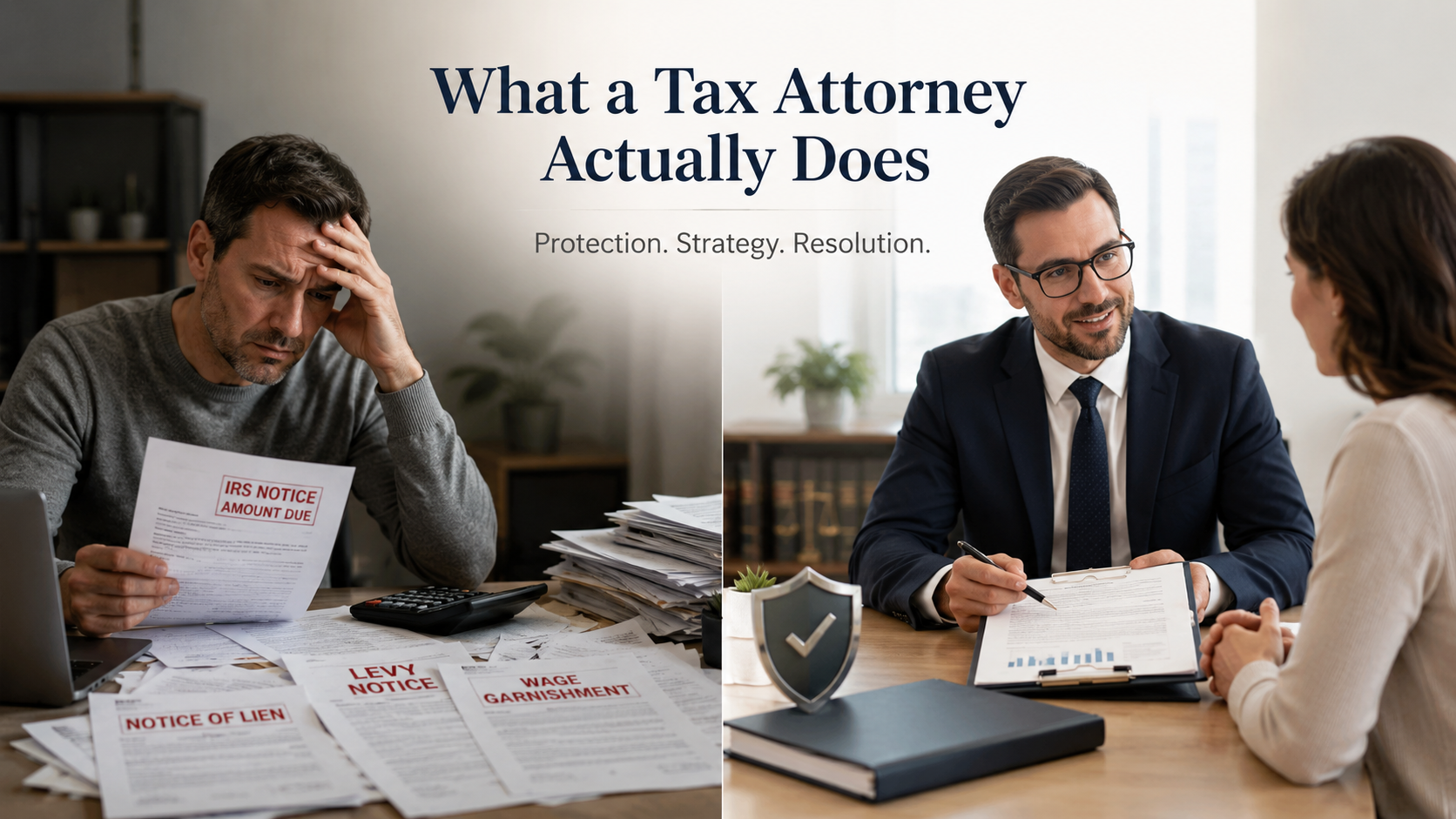

What a Tax Attorney Actually Does That General Advice Leaves Out

The IRS collected over $104 billion through enforcement actions in fiscal year 2023, according to the IRS Data Book — and that number does not include the penalties and interest quietly compounding on accounts that haven't been touched yet. If you're sitting on unresolved tax debt right now, the clo

Attorney Daniel Heller to Present at MVLS Tax Controversy Training

Tax controversy problems often begin with something that looks routine: a letter, a balance due, a delayed refund, a denied credit, or a question from the IRS or a state tax agency. But these issues can move quickly. What starts as paperwork can become an audit, a collection case, a lien, a levy, a

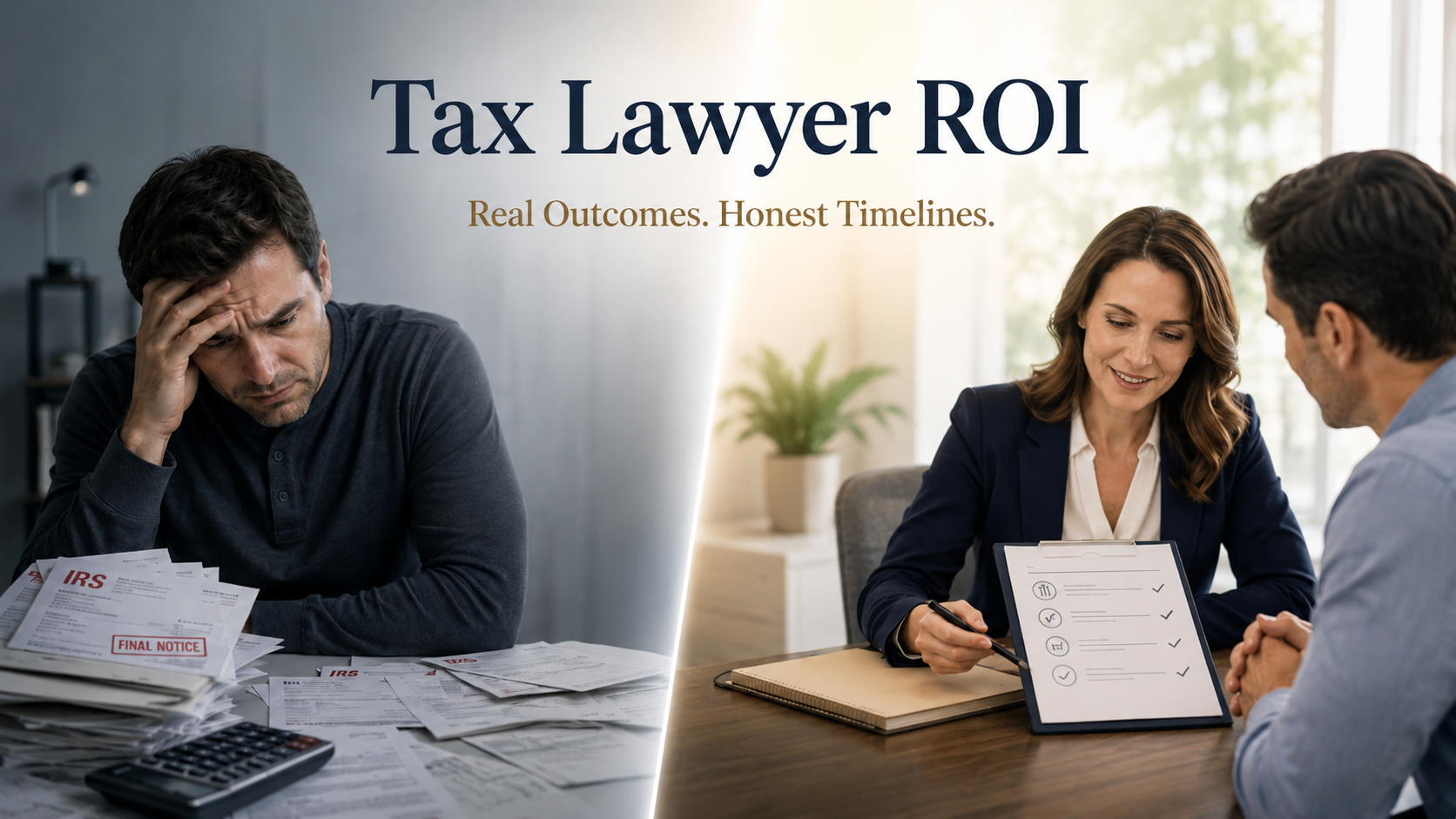

What Does Hiring a Tax Lawyer Actually Get You? Real ROI, Honest Timelines, and What Drives the Difference

The IRS collected over $98.4 billion through enforcement actions in fiscal year 2023, according to the IRS Data Book — and most of that came from people who waited too long, responded wrong, or tried to handle it alone. If you're sitting on unresolved tax debt right now, that number isn't abstract.

Why Conventional Tax Resolution Approaches Fail — And What Actually Stops the IRS

The IRS collected over $98 billion through enforcement actions in fiscal year 2022, according to the IRS Data Book — and the taxpayers who lost the most were not the ones with the biggest debts. They were the ones who waited, guessed, or trusted the wrong process. Direct Answer Conventional tax reso

Why IRS Defense Feels Harder Than It Should — And What Actually Resolves It

Direct Answer IRS defense feels harder than it should because the system is designed for compliance, not resolution — and most taxpayers approach it without understanding the procedural windows that control their options. The right intervention, at the right stage, stops collections, releases liens,

What the IRS Does When You Stop Filing Taxes

If you are wondering what happens if you stop filing taxes, realizing you have fallen years behind on your tax returns is a terrifying experience. Many taxpayers who stop filing taxes miss a single year due to a sudden life event, only to find that the paralyzing fear of what they might owe the IRS

IRS Bank Levy: What It Is, How It Works, and How to Stop It

Waking up to find your funds suddenly inaccessible due to an IRS bank account freeze can be a paralyzing financial shock. An IRS bank levy is a sudden, legal seizure of your property designed to satisfy an outstanding tax debt. Unlike a wage garnishment that takes a portion of your income over time,

How to Stop IRS Wage Garnishment Fast in Pennsylvania & New Jersey

Discovering a significantly reduced paycheck due to an IRS wage garnishment in PA or NJ can disrupt your ability to cover basic living expenses. Unlike private creditors in Pennsylvania and New Jersey, who typically need a court order, the IRS can bypass a judge and seize a substantial portion of yo

IRS Tax Debt Settlement: Your Options Explained

Receiving an IRS notice demanding thousands of dollars in back taxes is a stressful experience. For U.S. taxpayers navigating the federal tax system, the fear of escalating penalties, collection actions, and potential bank levies or wage garnishments can create anxiety. In the search for a way out,

What Should I Do if I Can’t Afford to Pay the IRS?

Opening a tax bill from the federal government that you cannot afford to pay is a stressful experience. For many individual taxpayers and self-employed people, realizing they lack the funds to cover their tax liability creates immediate anxiety about their financial security. However, letting that a

What Should I Do If I Owe the IRS More Than $10,000?

Discovering you owe the federal government a significant amount of money is an isolating experience. For many individuals and business owners, seeing a tax balance cross the five-figure mark creates immediate stress. However, letting that stress turn into inaction only makes the situation harder to

How Can I Reduce My IRS Tax Debt Legally?

Facing overwhelming IRS tax debt can feel like drowning in quicksand. Every day you wait, penalties and interest continue to pile up, making your situation worse. But here's what the IRS doesn't want you to know: you have LEGAL options to significantly reduce or eliminate your tax debt. The key is u

7 Mistakes You're Making with Delaware Franchise Tax Problems (And How a Tax Attorney Can Fix Them)

Delaware might be famous for being business-friendly, but that doesn't mean navigating its franchise tax requirements is a walk in the park. This post is specifically about Delaware franchise taxes and the common mistakes business owners make with them. Every year, thousands of corporations and LLCs

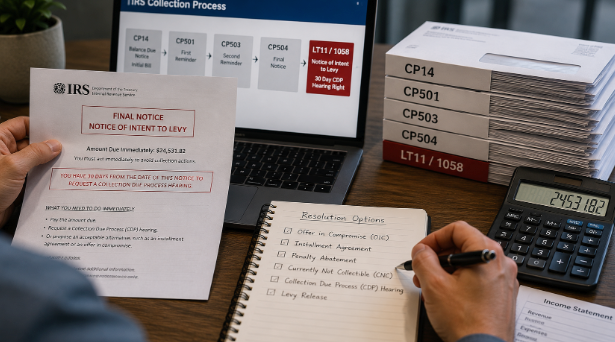

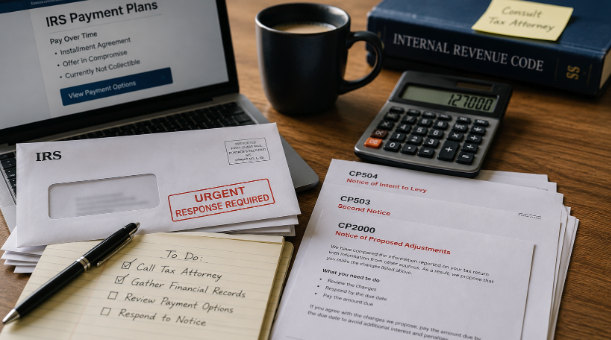

Ignored an IRS CP504 Notice? What Happens Next for Pennsylvania, New Jersey, and Maryland Taxpayers

Most IRS letters are easy to ignore. They arrive quietly, blend in with other mail, and don’t immediately change your day-to-day life. The CP504 notice is different — even though it may not feel urgent at first glance. Across Pennsylvania, New Jersey, and Maryland, we regularly speak with taxpayers

Why the IRS Thinks You Underreported Income — And How to Fix It Before It Becomes a Bigger Problem

Across Pennsylvania, South Jersey, and Maryland, thousands of taxpayers receive IRS notices each year stating that they underreported income. These notices show up in Philadelphia, Montgomery County, Bucks County, Delaware County, Camden County, Gloucester County, Cherry Hill, and throughout Marylan

Why the IRS Says You Owe More Than You Expected: A Tri-State Explanation

Pennsylvania, New Jersey, and Maryland taxpayers are seeing a rise in letters showing unexpected balances. These notices usually come from IRS data checks and automatic corrections. 1. Cross-State Income Issues Commuters who work across state lines often trigger mismatched withholding or inaccurate

Can You Really Settle IRS Tax Debt for Less Than You Owe? A Pennsylvania & New Jersey Deep Dive

IRS Problems in PA & NJ Don’t Happen Overnight People rarely end up with IRS tax debt because they’re irresponsible. The more common story across Pennsylvania and New Jersey is far more human: A job change leads to a gap in withholding.A family emergency drains savings.A business slows down.Divorce

Showing 1–27 of 828 articles

Beyond the blog

Hire us, don't just read about it

Criminal Tax Issues

When the government wants to put you in a cage — we put ourselves between you and them.

Tax Resolution Services

The IRS has lawyers. So should you.

IRS Collections Defense

When the IRS stops asking and starts taking — there's a legal counter to every move.

Additional Tax Services

Specialty tax matters — bankruptcy, foreign accounts, estate planning, payroll, gambling, and more.

More from the resource library